Foreign Accounts and Assets Can Create Reporting Obligations Many Taxpayers Never Realize Exist

Many U.S. taxpayers are surprised to learn that foreign bank accounts, investment accounts, retirement accounts, business accounts, and other financial assets located outside the United States create annual reporting obligations even when little or no tax is owed.

Many U.S. taxpayers are surprised to learn that foreign bank accounts, investment accounts, retirement accounts, business accounts, and other financial assets located outside the United States create annual reporting obligations even when little or no tax is owed.

For some, the issue arises after accepting a new job overseas, opening an account in another country, inheriting assets from a family member, maintaining accounts while living abroad, or acquiring an ownership interest in a foreign business. Others discover the requirement only after speaking with a tax professional, preparing a tax return, or receiving correspondence from the IRS regarding foreign financial assets.

In many cases, the concern is not whether taxes were paid. The issue is whether required foreign account and asset reporting obligations were satisfied. Understanding whether FBAR reporting applies, evaluating any potential exposure, and identifying available compliance options are often the first steps toward protecting your financial position and resolving uncertainty.

Allen Barron assists individuals, business owners, expatriates, dual citizens, and taxpayers with international financial interests in evaluating FBAR reporting requirements, addressing missed filings, and developing practical strategies for compliance with U.S. foreign account reporting laws.

Who Needs to Consider FBAR Reporting?

FBAR reporting requirements apply to more people than many taxpayers realize. While foreign bank accounts are often the first thing that comes to mind, reporting obligations may arise whenever a U.S. person has a financial interest in, or signature authority over, certain foreign financial accounts whose aggregate value exceeds applicable reporting thresholds.

Individuals who should consider whether FBAR reporting applies include:

Individuals who should consider whether FBAR reporting applies include:

- S. citizens living abroad

- green card holders

- dual citizens

- expatriates

- foreign nationals who have become U.S. tax residents

and individuals who maintain financial accounts outside the United States. Business owners with foreign operations, executives with authority over international accounts, and individuals who have inherited foreign assets may also have reporting obligations.

Many FBAR issues arise in situations that seem routine at the time. A taxpayer may retain accounts in their country of origin after moving to the United States, maintain local banking relationships while working overseas, inherit foreign financial assets from a parent or relative, or acquire ownership interests in foreign businesses and investment accounts. Others discover potential reporting obligations years later during tax preparation, estate administration, business transactions, or discussions with a financial advisor.

Because FBAR requirements are based upon specific facts and circumstances, determining whether reporting is required often begins with a careful review of foreign accounts, ownership interests, signature authority, and prior filing history. Understanding whether FBAR obligations exist is an important first step toward maintaining compliance and addressing potential issues before they become larger concerns.

Do Foreign Account Reporting Requirements Potentially Apply to You?

FBAR reporting requirements commonly apply to U.S. citizens, green card holders, tax residents, businesses, trusts, and other U.S. persons who have a financial interest in, or signature authority over, foreign financial accounts.

FBAR reporting requirements commonly apply to U.S. citizens, green card holders, tax residents, businesses, trusts, and other U.S. persons who have a financial interest in, or signature authority over, foreign financial accounts.

In general, FBAR reporting should be considered whenever the combined value of foreign financial accounts exceeds $10,000 at any point during the calendar year, even for a single day in that year. The requirement may apply even when no tax is owed and even when the accounts produce little or no income.

Foreign bank accounts, investment accounts, certain retirement accounts, business accounts, and other foreign financial accounts may all create reporting obligations under U.S. law.

Because reporting requirements depend upon specific facts and circumstances, many taxpayers first become aware of FBAR obligations only after opening a foreign account, inheriting assets overseas, living abroad, owning an international business, or discussing their situation with a tax professional.

The Most Important Thing You Need to Know About FBAR Compliance

Many taxpayers discover potential FBAR reporting obligations years after opening a foreign account, inheriting assets overseas, moving to or from another country, or acquiring an interest in a foreign business. In many cases, the issue is not intentional non-compliance. The reporting requirement was simply unknown.

Many taxpayers discover potential FBAR reporting obligations years after opening a foreign account, inheriting assets overseas, moving to or from another country, or acquiring an interest in a foreign business. In many cases, the issue is not intentional non-compliance. The reporting requirement was simply unknown.

The most important thing to understand is that waiting rarely improves the situation. Once a potential reporting issue is identified, taking action to understand your obligations and evaluate available compliance options often provides more flexibility and greater certainty than delaying the decision.

Every situation is different. Some taxpayers may have ongoing reporting obligations. Others may need to address prior-year filings. Some may discover that additional international reporting requirements apply beyond FBAR. The appropriate path depends upon the facts, the filing history, and the specific circumstances involved.

Understanding where you stand today is often the first step toward protecting your financial interests, reducing uncertainty, and establishing a clear path forward. We invite you to learn more about the integrated services of Allen Barron and Janathan L. Allen APC, and how we can help you to resolve these challenges. You can connect with the chat button on your screen, contact us or call today to schedule a free consultation at 866-631-3470.

What Is an FBAR?

An FBAR, or Report of Foreign Bank and Financial Accounts, is an annual reporting requirement that applies to certain U.S. taxpayers with foreign financial accounts. The report is filed with the U.S. Treasury Department and is separate from a federal income tax return.

An FBAR, or Report of Foreign Bank and Financial Accounts, is an annual reporting requirement that applies to certain U.S. taxpayers with foreign financial accounts. The report is filed with the U.S. Treasury Department and is separate from a federal income tax return.

The purpose of FBAR reporting is to provide the government with information about foreign financial accounts held or controlled by U.S. persons. Because FBAR is a reporting requirement rather than a tax return, an obligation to file may exist even when little or no tax is owed.

Many taxpayers first encounter FBAR requirements after opening a foreign account, living abroad, inheriting assets overseas, or acquiring an interest in a foreign business.

Who Must File an FBAR?

FBAR reporting requirements apply to U.S. persons who possess signature authority or hold a financial interest in foreign financial accounts whose combined value exceed applicable reporting thresholds at any point during the year – even for one day.

Individuals and entities who commonly encounter FBAR filing requirements include:

- S. citizens

- Green card holders

- S. tax residents

- Dual citizens

- S. businesses

- Trusts and estates

- Individuals with signature authority over foreign accounts

Because reporting obligations depend upon specific facts and circumstances, determining whether an FBAR is required often begins with a review of account ownership, account values, and authority over foreign financial accounts.

What Accounts Must Be Reported?

The actual definition of a foreign financial account is broader than many taxpayers expect. Depending upon the circumstances, FBAR reporting requirements may apply to:

The actual definition of a foreign financial account is broader than many taxpayers expect. Depending upon the circumstances, FBAR reporting requirements may apply to:

- Foreign bank accounts

- Foreign brokerage accounts

- Foreign investment accounts

- Certain foreign retirement and pension accounts

- Certain foreign insurance products with cash value

- Joint foreign accounts

- Foreign business accounts

Accounts over which an individual has signature authority

Determining whether a particular account or group of accounts must be reported requires a careful review of the account(s), ownership interests, and the applicable reporting rules.

I Have Foreign Bank, Investment, or Cryptocurrency Accounts

If you maintain financial accounts outside the United States, the central issue is whether those accounts create a U.S. reporting obligation. By this point, the FBAR rules may already be clearer: the filing requirement is not limited to accounts that produce income, accounts held in one person’s name, or accounts that create tax due.

Foreign bank accounts, investment accounts, retirement accounts, joint accounts, business accounts, and certain foreign cryptocurrency accounts may all require careful review. The concern is not simply whether the account exists. The concern is whether the account should have been disclosed, whether the aggregate value crossed the reporting threshold, and whether prior-year filings were handled correctly.

If you were brought directly to this section from the top of the page, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file one, and what types of accounts must be reported.

What matters now is determining whether your accounts create a current or prior-year filing obligation, whether any income or asset reporting issues overlap with FBAR compliance, and what steps are available to protect your position before the matter becomes more difficult to resolve.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating available options, and protecting your financial interests.

Helpful Next Steps

→ Review FBAR Reporting Basics

→ Foreign Financial Investments

→ Cryptocurrency and Digital Asset Reporting

→ International Tax Planning for Individuals

→ International Tax Services

Living Outside the United States and FBAR Reporting Requirements

Many U.S. citizens living abroad are surprised to learn that relocating to another country does not automatically eliminate U.S. tax and financial reporting obligations. In fact, foreign accounts that become part of everyday life overseas are often the very accounts that create FBAR reporting requirements.

Local checking and savings accounts, retirement accounts, investment accounts, employer-sponsored financial plans, and other financial relationships established in a country of residence may all warrant review. What feels like a normal local banking relationship abroad may still create reporting obligations for a U.S. citizen, dual citizen, lawful permanent resident, or certain other U.S. persons.

The issue is often not whether income was earned or taxes were paid overseas. Instead, the question is whether required disclosures were completed correctly and whether all applicable international reporting obligations have been identified. Many expatriates discover these requirements years after moving abroad, often after opening multiple accounts, purchasing investments, or building retirement savings in their country of residence.

If you arrived here directly from the user pathway section, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file, and what types of accounts may be reportable.

What matters most now is determining which reporting obligations apply to your specific circumstances, whether prior-year filings were completed properly, and what options may be available if something has been overlooked. Many international reporting issues can be addressed proactively when identified early.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating available options, and protecting your financial interests.

Learn More About FBAR Reporting for U.S. Expats

→ Review FBAR Reporting Basics

→ International Tax Planning for U.S. Expatriates

→ Foreign Retirement Accounts and Reporting Requirements

→ Expatriate Hub

Inherited Foreign Assets and FBAR Reporting Requirements

Inheriting foreign assets can create U.S. reporting obligations that many beneficiaries never anticipate. In many cases, the inheritance itself is not the issue. The challenge is understanding whether inherited accounts, investments, or financial assets create ongoing disclosure requirements after ownership is transferred.

Foreign bank accounts, investment accounts, retirement assets, inherited family holdings, and other overseas financial interests may become subject to reporting requirements once a U.S. taxpayer acquires an ownership interest or gains authority over the assets. Many individuals discover these obligations only after reviewing estate documents, accessing inherited accounts, or speaking with financial institutions located outside the United States.

The situation can become even more complicated when inherited assets remain overseas, distributions occur over time, multiple family members share ownership interests, or foreign trusts and estate structures are involved. What appears to be a straightforward inheritance may involve reporting requirements that extend beyond a traditional income tax return.

If you arrived here directly from the user pathway section, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file, and what types of accounts may be reportable.

What matters most is understanding which reporting obligations apply to the inherited assets, whether required disclosures have been completed properly, and what options may be available if prior filings were overlooked. Many international reporting issues can be addressed proactively before they become more disruptive or expensive to resolve.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating available options, and protecting your financial interests.

Learn More About Inherited Foreign Accounts and Assets

→ Review FBAR Reporting Basics

→ Foreign Trust and Estate Reporting

→ International Tax Services for Individuals

→ International Tax Planning for Individuals

Foreign Business Ownership and International Reporting Requirements

Owning an interest in a foreign business may create reporting obligations that extend well beyond a traditional U.S. income tax return. Many business owners are surprised to discover that separate disclosure requirements can apply even when the company operates entirely outside the United States and all local filing requirements have been satisfied.

Foreign corporations, partnerships, limited liability entities, and other business structures may trigger various international reporting requirements depending upon the nature of the ownership interest, management authority, and financial relationships involved. In some situations, simply having signature authority over foreign business accounts can create reporting obligations independent of ownership.

The complexity often increases when a business maintains foreign bank accounts, conducts international operations, has multiple owners, reinvests earnings overseas, or operates through affiliated entities. Many business owners assume that because the company maintains its own records and files local returns, no additional U.S. reporting is required. Unfortunately, international reporting obligations frequently apply at both the business and individual level.

If you arrived here directly from the user pathway section, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file, and what types of accounts may be reportable.

What matters most is understanding which reporting obligations apply to the business, whether foreign accounts and ownership interests have been disclosed properly, and whether any prior-year reporting issues require attention. Many international compliance concerns can be addressed proactively before they become significantly more disruptive or costly to resolve.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of

understanding your reporting obligations, evaluating available options, and protecting your financial interests.

Learn More About Foreign Business Reporting Requirements

→ Review FBAR Reporting Basics

→ Foreign Business Ownership and Reporting

→ International Tax Planning for Business Owners

→ Foreign Corporations, Partnerships, and Entity Reporting

Recently Learning About FBAR Requirements

Many taxpayers first learn about FBAR reporting requirements years after opening foreign accounts, receiving inherited assets, moving overseas, or becoming involved with international investments or businesses. In many cases, the accounts have existed for years before anyone mentions the possibility of an FBAR filing obligation.

It is not uncommon for taxpayers to discover these requirements during a conversation with a CPA, while preparing a tax return, through online research, or after hearing about FBAR reporting from a financial advisor, family member, or colleague. For many individuals, the first reaction is uncertainty. Questions often arise about whether reporting obligations apply, whether prior filings were required, and what should be done next.

The most important thing to understand is that discovering a potential reporting issue does not automatically mean a taxpayer has done something wrong. Before making assumptions, it is important to determine whether an FBAR filing requirement actually existed, whether other international reporting obligations may apply, and what options are available based upon the specific facts and circumstances involved.

If you arrived here directly from the user pathway section, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file, and what types of accounts may be reportable.

What matters most now is gaining clarity. Understanding whether a filing obligation exists, evaluating any potential compliance concerns, and identifying available options early often provides a clearer path forward than reacting based on assumptions or incomplete information.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating available options, and protecting your financial interests.

Learn More About Understanding FBAR Requirements

→ Review FBAR Reporting Basics

→ FBAR Requirements for a U.S. Person for an Offshore Account

→ International Tax Compliance and Reporting

→ International Tax Planning

Missed FBAR Filings and Compliance Options

Many taxpayers discover potential FBAR filing issues years after foreign accounts were opened, inherited, or established as part of living, working, or investing abroad. In many situations, the accounts were never hidden, taxes may have been properly reported, and the individual simply did not know a separate FBAR filing requirement existed.

Missing an FBAR filing does not automatically mean fraud, tax evasion, or criminal conduct. The circumstances surrounding the omission matter. Understanding what happened, when reporting obligations arose, and whether the failure to file was inadvertent or based upon a lack of awareness is often an important first step in evaluating the situation.

Many taxpayers become aware of potential compliance issues after speaking with a CPA, preparing a tax return, researching foreign account reporting requirements, or learning about FBAR obligations for the first time. Others discover that foreign accounts have existed for years without the required disclosures ever being filed.

If you arrived here directly from the user pathway section, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file, and what types of accounts may be reportable.

What matters most now is understanding the scope of the issue, determining which years may be affected, evaluating available compliance options, and developing a strategy based upon the specific facts involved. Many taxpayers are able to address reporting issues proactively once they understand their obligations and available paths forward.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Assessment, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating available options, and protecting your financial interests.

Learn More About Missed FBAR Filings and Compliance Options

→ Review FBAR Reporting Basics

→ International Tax Services

→ Voluntary Compliance and Disclosure Options

→ International Tax Planning and Compliance

IRS Foreign Account Notices and Compliance Matters

Receiving correspondence from the IRS regarding foreign accounts, offshore reporting obligations, or international tax compliance can be unsettling. Many taxpayers are uncertain whether the notice relates to an FBAR filing issue, foreign asset reporting requirements, prior tax returns, or a request for additional information.

An IRS notice does not automatically mean wrongdoing has occurred. In many situations, the IRS is seeking clarification, requesting documentation, identifying a potential reporting discrepancy, or asking questions regarding foreign financial accounts or international disclosures. Understanding precisely what the notice says—and what it does not say—is often the first step in evaluating the situation.

Foreign account reporting issues can involve a variety of filing requirements, including FBAR disclosures, foreign asset reporting, international information returns, and related compliance matters. The nature of the notice, the years involved, and the taxpayer’s reporting history often influence both the scope of the issue and the options available moving forward.

If you arrived here directly from the user pathway section, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file, and what types of accounts may be reportable.

What matters most now is understanding the issues being raised, reviewing prior filings and reporting obligations, identifying any potential compliance concerns, and evaluating available response strategies before deadlines pass or additional complications arise.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Assessment, or call (866) 631-3470 to begin the process of understanding the issues presented, evaluating available options, and protecting your financial interests.

Learn More About IRS Foreign Account Notices and Compliance Matters

→ Review FBAR Reporting Basics

→ IRS International Tax Notices and Responses

→ FBAR Penalties and Enforcement

→ International Tax Compliance and Reporting

Becoming Compliant with FBAR Reporting Requirements

Many taxpayers seek guidance not because they have received a government notice or are facing an immediate enforcement action, but because they want to understand their obligations and address potential reporting issues before they become more complicated.

Some individuals recently discovered FBAR reporting requirements and want to determine whether they apply. Others are aware that prior filings may have been missed and want to evaluate available compliance options. Still others are looking for a clear process to manage ongoing reporting obligations associated with foreign accounts, international investments, inherited assets, or overseas business interests.

In many situations, addressing reporting obligations before government contact provides greater flexibility, more available options, and a clearer understanding of potential risks. Taking proactive steps often allows taxpayers to evaluate their circumstances carefully, gather necessary information, and establish a strategy designed to address both past and future reporting requirements.

If you arrived here directly from the user pathway section, it may be helpful to first review the FBAR reporting basics, including what an FBAR is, who must file, and what types of accounts may be reportable.

What matters most now is understanding your reporting obligations, evaluating any prior-year compliance concerns, and developing a practical plan for moving forward. Many international reporting issues can be resolved more effectively when they are identified and addressed before additional questions, notices, or enforcement actions arise.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating available compliance options, and protecting your financial interests.

Learn More About Becoming Compliant with FBAR Reporting Requirements

→ Review FBAR Reporting Basics

→ FBAR Compliance and Filing Requirements

→ Voluntary Compliance and Disclosure Options

→ International Tax Planning and Compliance

Why Experience Matters in FBAR Preparation and Compliance

Why Experience Matters in FBAR Preparation and Compliance

FBAR compliance issues often appear deceptively simple. A taxpayer may believe the question is merely whether a foreign account should have been reported. In reality, many FBAR matters involve a broader analysis of account ownership, signature authority, aggregate account balance analysis, reporting thresholds, international tax filings, prior-year compliance history, and the circumstances surrounding any missing or incomplete disclosures.

Did the aggregate value of all foreign accounts exceed reporting thresholds at any point during the year, even for a single day?

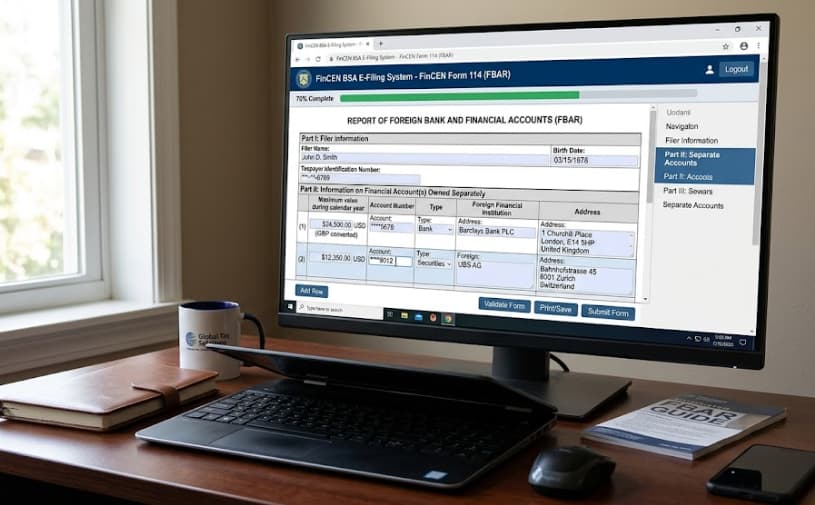

Many taxpayers are surprised to learn that FBAR reporting is not filed with the IRS. Instead, FBAR disclosures are submitted to the Financial Crimes Enforcement Network (FinCEN).

The IRS maintains separate international reporting requirements that may apply to foreign financial assets and offshore accounts. In some situations, a taxpayer may be required to file both an FBAR and additional IRS reporting forms. Because reporting thresholds, filing requirements, and definitions differ, international compliance issues can become more complex than many individuals initially realize. A taxpayer may satisfy one reporting obligation while overlooking another. What appears to be a relatively modest foreign account balance or ordinary overseas financial relationship may nevertheless create multiple reporting obligations under U.S. law.

Foreign account reporting obligations frequently intersect with other international reporting requirements. A taxpayer may have FBAR filing obligations, foreign asset disclosures, international information returns, foreign business reporting requirements, or international tax issues that must be evaluated together rather than in isolation. What initially appears to be a single filing question can quickly become a much broader compliance matter.

Experience matters because FBAR compliance requires more than preparing and filing forms. It requires understanding how international reporting rules interact, recognizing potential compliance risks, evaluating available options when prior filings have been missed, and helping taxpayers make informed decisions before unnecessary penalties or complications arise. Early decisions often influence the options available later.

International Investments, Accounts, Real Estate, and Business Interests Require Expert Insight from Multiple Disciplines

The value of integrated tax, legal, accounting, and business advisory services cannot be overstated for individuals and businesses with foreign accounts, offshore assets, international investments, and cross-border business interests.

The value of integrated tax, legal, accounting, and business advisory services cannot be overstated for individuals and businesses with foreign accounts, offshore assets, international investments, and cross-border business interests.

International reporting and compliance issues rarely exist within a single professional discipline. A decision that appears appropriate from a legal perspective may create unintended tax consequences.

A tax-driven strategy may create accounting complications. A business decision may trigger reporting obligations that were never anticipated. When multiple advisors operate independently, each may provide sound advice within their area of expertise while no one evaluates the full picture.

That is one of the reasons clients value the integrated structure of Allen Barron, Inc. and Janathan L. Allen, APC. Rather than coordinating separate conversations among multiple professionals, clients gain access to a team capable of evaluating legal, tax, accounting, financial, and business considerations together. The result is often greater clarity, better decision-making, reduced risk, improved efficiency, and opportunities that might otherwise be overlooked.

For many clients, the ability to have a single conversation with Janathan Allen and the Allen Barron team provides meaningful value in itself. Complex international reporting matters become easier to understand, options become easier to evaluate, and decisions can be made with a clearer understanding of the consequences across all aspects of the client’s financial and business life.

International reporting obligations frequently extend beyond a single filing requirement. They often involve overlapping tax, legal, accounting, financial, and business considerations that must be evaluated together. This is one of the reasons integrated professional guidance can be particularly valuable in complex FBAR and international compliance matters.

We invite you to access our chat module, Schedule Your Complimentary Assessment, or call (866) 631-3470 to begin the process of understanding the complex financial, reporting, legal, and tax issues presented, evaluating available options, and protecting your personal, business, legal, and financial interests.

Why Integrated Legal, Tax, and Accounting Matters

Many international tax and reporting issues are not isolated problems. They often involve overlapping legal, tax, accounting, reporting, financial, and business considerations that affect one another in important ways.

A foreign account may trigger multiple reporting obligations.

An international investment may create tax and compliance consequences.

A foreign business interest may affect reporting requirements, ownership structure, and long-term planning.

A legal decision may materially impact taxation, asset protection, reporting obligations, or future business objectives.

The challenge is that many professionals evaluate these issues from only one perspective.

An integrated approach helps identify not only the immediate issue, but the underlying legal, tax, accounting, reporting, financial, and business considerations that may ultimately shape the outcome moving forward.

That integration has long been one of the defining advantages of Allen Barron’s approach to complex international tax, legal, accounting, financial, and business matters.

Many international reporting and compliance concerns initially appear to be isolated issues. In reality, they are often symptoms of a larger underlying challenge.

The old expression, “where there’s smoke, there’s fire,” frequently applies.

A taxpayer may believe they simply need assistance with an FBAR filing, foreign asset disclosure, international investment, foreign business interest, or IRS reporting issue. As the situation is examined more closely, other legal, tax, accounting, reporting, operational, and strategic considerations often emerge beneath the surface.

An integrated approach helps identify not only the visible issue, but the underlying factors that may ultimately determine risk, opportunity, compliance, and long-term outcomes moving forward.

![]()

You Need an Advisor You Can Trust — A Single Phone Call to Make When Challenges and Opportunities Arise

International reporting obligations, foreign accounts, offshore investments, cross-border business interests, and international tax matters often create questions that extend beyond a single form, filing requirement, or tax return. The challenge is rarely finding information. The challenge is understanding how legal, tax, accounting, reporting, financial, and business considerations interact and what actions make sense moving forward.

Janathan L. Allen and the team at Allen Barron provide integrated legal, tax, accounting, and business advisory services designed to help individuals, investors, business owners, expatriates, and international taxpayers navigate complex financial and reporting matters with greater clarity and confidence.

Whether you are attempting to understand FBAR requirements, address prior-year compliance concerns, evaluate international reporting obligations, respond to government inquiries, structure an international investment, or simply gain confidence that your reporting obligations have been addressed properly, experienced guidance can help you better understand your options before important decisions are made.

The initial consultation is a substantive, confidential discussion designed to help you understand your current situation, identify potential risks and opportunities, evaluate available options, and determine appropriate next steps.

You are invited to engage the chat module on this page, contact Allen Barron, or call (866) 631-3470 to schedule your complimentary consultation.

Learn more about Janathan L. Allen, APC and Allen Barron’s integrated legal, tax, accounting, and business advisory services and how an integrated approach may help identify opportunities, reduce unnecessary risk, protect assets, and support your long-term financial and business objectives.

Learn more about Janathan L. Allen, APC and Allen Barron’s integrated tax, legal, accounting and business consulting services and how an integrated approach may help identify risk, protect assets, reduce unnecessary exposure, and support your long-term business and financial objectives.