International tax issues often arise when people, businesses, money, investments, property, or ownership interests cross borders. A foreign bank account creates U.S. reporting obligations for a U.S. taxpayer. An overseas business investment may affect tax filings in multiple countries. Relocating to or from the United States can trigger residency, reporting, and planning considerations that extend well beyond a single tax return.

International tax issues often arise when people, businesses, money, investments, property, or ownership interests cross borders. A foreign bank account creates U.S. reporting obligations for a U.S. taxpayer. An overseas business investment may affect tax filings in multiple countries. Relocating to or from the United States can trigger residency, reporting, and planning considerations that extend well beyond a single tax return.

Many international tax matters involve multiple jurisdictions, overlapping reporting requirements, and financial activities that span countries with different tax systems, regulations, and compliance expectations. What appears to be a straightforward transaction in one country may create additional reporting obligations, tax consequences, or planning opportunities in another.

In addition, many countries throughout the world apply the International Financial Reporting Standards (IFRS) accounting framework. This differs significantly from the U.S. Generally Accepted Accounting Principles (GAAP) standard. A substantial component of many international tax matters involves reconciling, translating, or reconstructing accounting information prepared under foreign accounting standards so it can be used for U.S. reporting, financial statement, and tax compliance purposes.

In many respects, international tax matters resemble an international airport.

People arrive from different countries, headed toward different destinations, carrying different goals and concerns. Some are planning future investments, business ventures, or residency changes. Others are responding to an IRS notice, addressing unreported foreign accounts, evaluating international business structures, or resolving compliance concerns involving foreign assets and reporting requirements.

The airport’s responsibility is not to determine where every traveler should go. Its responsibility is to provide orientation, connect systems, and help people identify the path that best fits their destination.

The same is often true of international tax planning, compliance, and controversy matters.

Understanding which reporting obligations apply, what risks may exist, and which decisions could carry long-term consequences is often the first step toward protecting your financial interests. Whether you own foreign assets, operate an international business, live abroad, invest in the United States, or are addressing international reporting concerns, informed decisions begin with understanding the landscape you have entered.

Allen Barron provides integrated tax, legal, accounting, estate planning, and business advisory services designed to help individuals and businesses navigate complex international tax environments. The integrated protections of the attorney-client privilege cannot be overstated in the context of international tax matters.

The purpose of this page is to help you understand the issues that may affect your situation, identify potential areas of concern, and connect with information relevant to your specific circumstances.

What Is the Most Important Thing You Need to Know Right Now?

International tax problems rarely begin when a tax return is filed. More often, they begin when an account is opened, an investment is made, a business is formed, property is acquired, money is transferred, a trust is established, or residency changes occur without fully understanding the reporting and tax consequences that may follow.

In many cases, the greatest risks are not created by intentional misconduct, but by a lack of awareness. Foreign accounts, overseas investments, business ownership interests, gifts, inheritances, trusts, and cross-border transactions can trigger reporting obligations and compliance requirements that are not immediately obvious to individuals, families, and business owners.

If there is something you have missed, overlooked, or only recently discovered, it is often possible to address the issue and improve compliance before more significant consequences arise.

The good news is that international tax matters often present opportunities to address concerns, improve compliance, reduce risk, and identify planning options before problems become more difficult, expensive, or disruptive to resolve.

Understanding what obligations may apply, what decisions matter most, and what steps can be taken now is often the first step toward protecting your financial interests, preserving future opportunities, and achieving the best possible outcome.

Foreign Accounts, Assets, and International Reporting

Owning foreign bank accounts, investment accounts, retirement assets, real estate, business interests, or other overseas financial assets does not automatically create a tax problem. However, U.S. taxpayers may be subject to reporting and disclosure requirements that apply even when little or no tax is owed.

International reporting obligations arise in many ways. A foreign bank account may trigger FBAR reporting requirements. Foreign financial assets may require FATCA disclosures. Ownership interests in foreign businesses, trusts, partnerships, or investments may create additional reporting obligations that extend beyond a traditional tax return. In many cases, taxpayers are surprised to learn that reporting requirements can apply even when assets generate little income or are held entirely outside the United States.

What matters most is often understanding which reporting obligations apply, whether prior filings were completed correctly, and what options may be available if something has been missed or overlooked. Many international reporting issues can be addressed proactively before they become more complicated, disruptive, or expensive to resolve.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Assessment, or call (866) 631-3470 to begin the process of understanding your obligations, evaluating available options, and protecting your financial interests.

Learn More About Foreign Accounts, Assets, and International Reporting

→ FBAR Reporting and Compliance

→ Foreign Financial Investments

→ Offshore Financial Account Reporting and Compliance

→ International Tax Planning for Individuals

Living Abroad and International Tax Planning

The United States taxes its citizens and U.S. taxpayers on all income worldwide. Moving overseas does not end a taxpayer’s obligations to the United States. U.S. citizens and certain residents remain subject to ongoing filing, reporting, and disclosure requirements involving foreign income, bank accounts, investments, retirement assets, business interests, and other international financial activities.

International tax issues often arise before a move abroad, during the transition itself, and long after residency has changed. Questions involving tax residency, foreign earned income, retirement planning, international investments, foreign account reporting, and long-term compliance obligations frequently affect individuals living, working, retiring, or conducting business outside the United States. In many cases, proactive planning can help identify opportunities, reduce compliance risks, and avoid unexpected reporting issues in the future.

What matters most is often understanding how U.S. tax rules continue to apply, what reporting obligations may exist, and how major financial and residency decisions could affect long-term tax outcomes. The earlier these issues are evaluated, the more options are typically available for planning and compliance.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of understanding your international tax obligations, evaluating planning opportunities, and protecting your financial interests.

Learn More About International Tax Planning for U.S. Citizens Living Abroad

→ U.S. Citizens Living Abroad

→ Expatriate Tax Services

→ International Tax Planning and Compliance

→ Foreign Account Reporting Requirements

→ Expatriate Information Hub

Moving to the United States and Investing in U.S. Opportunities

Relocating to the United States, investing in American businesses, acquiring U.S. real estate, or establishing a business presence within the United States can create tax obligations that differ significantly from those imposed in other countries. Residency rules, entity selection, investment structures, income sourcing rules, and reporting requirements may all influence the long-term financial impact of a move or investment.

International investors and foreign nationals are often surprised to discover that activities involving U.S. assets, businesses, and income can trigger tax and reporting obligations that extend beyond a single transaction. Decisions regarding how assets are acquired, how businesses are structured, where income is earned, and how investments are managed can have lasting consequences for both tax compliance and long-term planning. Early evaluation frequently helps identify opportunities, avoid unnecessary complications, and support informed decision-making.

What matters most is often understanding how U.S. tax laws apply to your specific circumstances, what reporting obligations may exist, and how major financial decisions may affect future tax exposure. Planning before a move, acquisition, or investment is often far easier than correcting avoidable issues after they occur.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of understanding your U.S. tax obligations, evaluating available planning opportunities, and protecting your financial interests.

Learn More About U.S. Tax Planning for Foreign Nationals and International Investors

→ Foreign Nationals Investing in the United States

→ International Tax Planning for New U.S. Residents

→ Cross-Border Investment and Tax Planning

Foreign Business Ownership and International Tax Compliance

Owning, operating, or investing in a foreign corporation, partnership, joint venture, or other business entity can create reporting obligations that extend far beyond the business’s day-to-day operations. U.S. taxpayers with foreign ownership interests are often subject to specialized disclosure requirements, compliance obligations, and tax rules that may apply even when the business generates little income or operates entirely outside the United States.

International business ownership frequently involves complex relationships between the business, its owners, foreign jurisdictions, and U.S. tax authorities. Decisions involving ownership structure, distributions, investments, expansion, succession planning, and cross-border transactions can affect both business operations and long-term tax outcomes. In many cases, understanding these obligations early helps reduce risk, improve compliance, and identify opportunities for more effective planning.

Foreign business ownership may also require the evaluation of financial information prepared under foreign accounting standards, including IFRS and other international reporting frameworks, to support U.S. tax reporting and compliance obligations.

What matters most is often understanding how foreign business ownership affects U.S. reporting requirements, what obligations apply to owners and investors, and whether existing structures continue to support the organization’s long-term objectives. Proactive evaluation often helps prevent small compliance issues from becoming more significant concerns.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of evaluating your reporting obligations, identifying planning opportunities, and protecting your business and financial interests.

Learn More About Foreign Business Ownership and International Tax Compliance

→ Foreign Corporation Reporting

→ International Business Structures

→ Transfer Pricing Issues

→ Foreign Partnership Reporting

→ International Tax Planning for Business Owners

→ Cross-Border Business Compliance

International Business Operations and Cross-Border Tax Planning

Businesses that operate across international borders often encounter tax, accounting, regulatory, and reporting issues that do not arise in purely domestic operations. Whether a company buys, sells, manufactures, licenses, employs, contracts, or provides services internationally, activities spanning multiple jurisdictions may create additional obligations and planning considerations that affect both daily operations and long-term business strategy.

Cross-border business activities frequently involve foreign subsidiaries, related-party transactions, international expansion, intellectual property considerations, and financial information prepared under different accounting and reporting standards. As organizations grow internationally, decisions regarding structure, operations, reporting, and compliance can significantly influence tax exposure, regulatory risk, and future opportunities.

Cross-border business ownership may also require the evaluation of financial information prepared under foreign accounting standards, including IFRS and other international reporting frameworks, to support U.S. tax reporting and compliance obligations.

What matters most is often understanding how international operations affect the organization as a whole, what obligations exist across the jurisdictions involved, and whether existing structures continue to support the company’s objectives. Early planning and ongoing evaluation frequently help businesses identify opportunities, maintain compliance, and avoid unnecessary disruption as international operations evolve.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Consultation, or call (866) 631-3470 to begin the process of evaluating your international operations, identifying planning opportunities, and protecting your business interests.

Learn More About International Business Operations and Cross-Border Tax Planning

→ International Business Expansion

→ Cross-Border Transactions

→ Foreign Subsidiaries and Related-Party Transactions

→ International Tax Planning for Businesses

→ International Accounting and Compliance Considerations

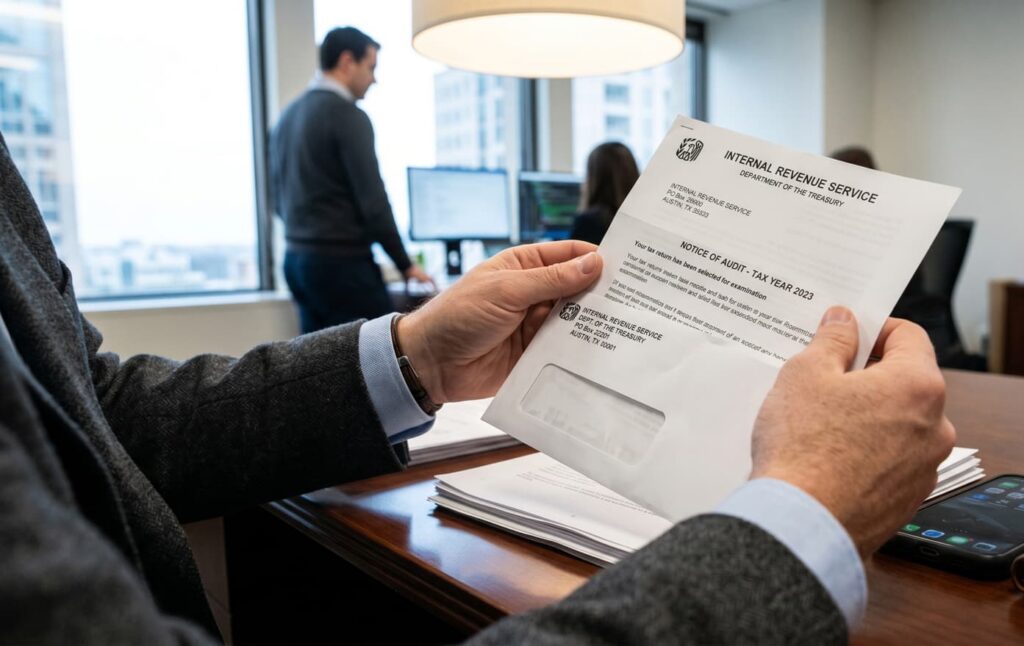

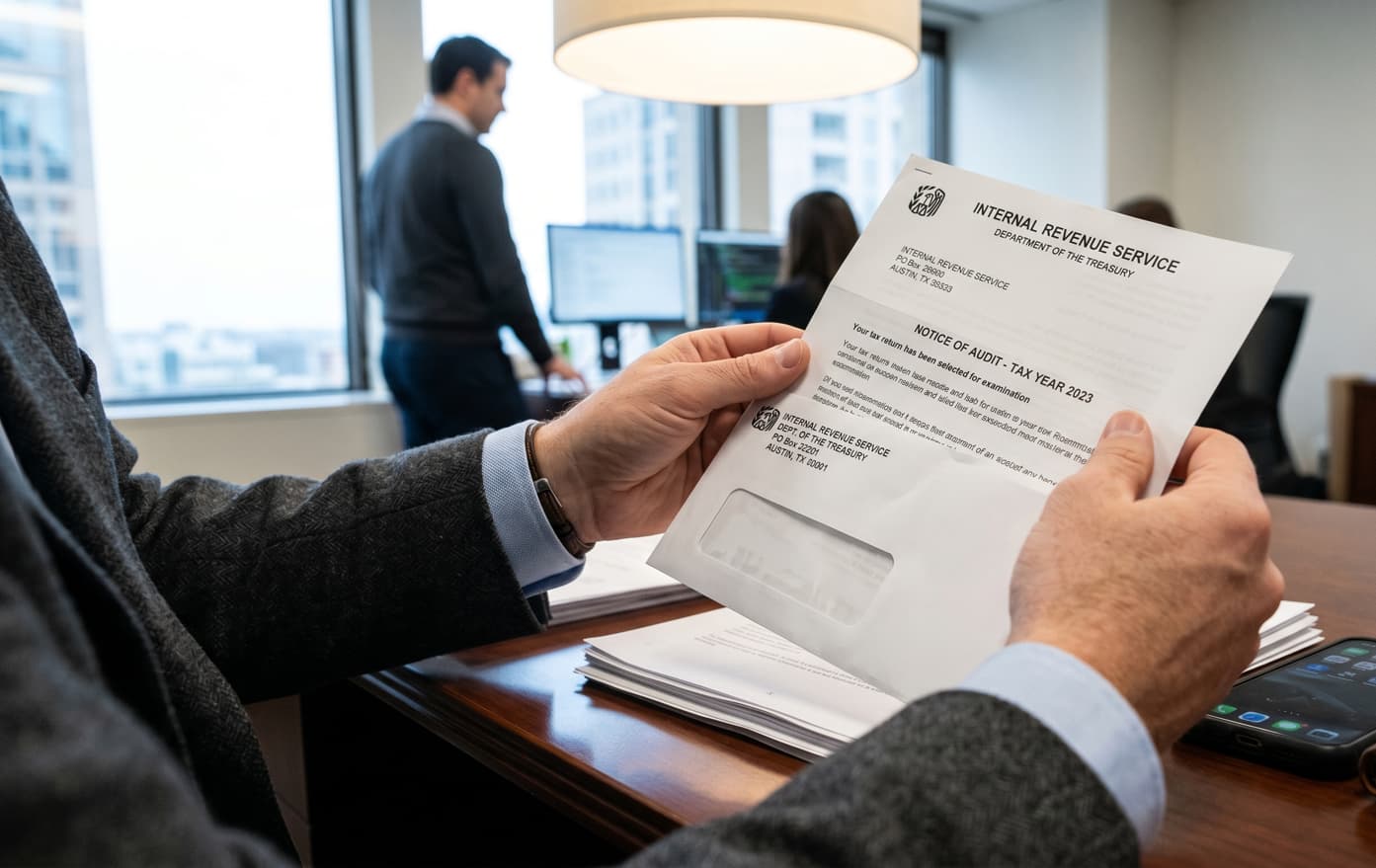

International Tax Compliance, Voluntary Disclosure, and IRS Notices

Receiving an IRS notice, discovering a missed filing requirement, or learning that foreign accounts, assets, businesses, trusts, or investments may not have been properly reported can create understandable concern. International tax compliance issues often involve specialized reporting requirements, significant penalties, and important decisions regarding how past filings and ongoing obligations should be addressed.

Many international reporting issues arise not because a taxpayer intentionally failed to comply, but because the reporting requirements were unfamiliar or overlooked. Foreign bank accounts, offshore investments, foreign business interests, trusts, gifts, inheritances, and other international financial activities can trigger disclosure obligations that are not always obvious. In many situations, taxpayers have opportunities to evaluate available compliance options, correct prior reporting issues, and improve their position before matters become more complicated or enforcement activity escalates.

What matters most is often understanding the nature of the reporting issue, identifying which obligations apply, evaluating available compliance pathways, and developing a strategy that protects both legal and financial interests. Early evaluation frequently provides the greatest flexibility and the broadest range of available options.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Assessment, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating available compliance options, and protecting your financial interests.

Learn More About International Tax Compliance, Voluntary Disclosure, and IRS Notices

→ IRS International Tax Notices

→ FBAR Compliance and Reporting

→ Offshore Account Compliance

→ International Voluntary Disclosure Options

Foreign Gifts, Inheritances, Trusts, and International Property Ownership

Receiving a foreign gift, inheritance, or trust distribution, or owning real estate located outside the United States, does not automatically create a tax problem. However, these situations can trigger reporting obligations, disclosure requirements, and planning considerations that are often unfamiliar to individuals and families managing international assets.

Many taxpayers are surprised to learn that foreign gifts, inherited property, trust interests, and overseas real estate holdings may create reporting requirements even when little or no immediate tax is owed. Ownership structures, trust arrangements, future income generated by the assets, and eventual transfers or sales can all affect long-term compliance obligations and financial planning decisions. Understanding these issues early often helps preserve valuable opportunities while reducing the risk of unnecessary reporting problems.

What matters most is often understanding how the assets are owned, what reporting requirements may apply, and how future decisions could affect tax obligations, estate planning objectives, and long-term financial outcomes. Early evaluation frequently helps individuals and families make informed decisions while protecting both assets and future options.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Assessment, or call (866) 631-3470 to begin the process of understanding your reporting obligations, evaluating planning opportunities, and protecting your financial interests.

Learn More About Foreign Gifts, Inheritances, Trusts, and International Property Ownership

→ Foreign Gift Reporting Requirements

→ International Inheritance Issues

→ Foreign Trust Reporting and Compliance

→ Foreign Real Estate Ownership

→ International Estate and Succession Planning

Expatriation, Exit Planning, and International Residency Changes

Major residency changes, long-term international relocation, and expatriation decisions can have tax consequences that extend well beyond the move itself. Changes in tax residency, citizenship status, asset ownership, business interests, retirement planning, and future reporting obligations may all affect long-term financial outcomes. Because these decisions often involve multiple jurisdictions, careful planning is frequently an important part of protecting both assets and future opportunities.

Many individuals considering expatriation or significant international residency changes are evaluating more than taxes alone. Business ownership, investment holdings, estate planning objectives, retirement considerations, family circumstances, and future reporting obligations often intersect in ways that require thoughtful analysis before major decisions are made. In many cases, opportunities that exist before a move or expatriation event may become more limited once the transition has occurred.

What matters most is often understanding how residency changes may affect current and future tax obligations, identifying planning opportunities before important decisions are finalized, and evaluating how international assets and business interests fit within long-term financial objectives. Early planning frequently provides greater flexibility, more options, and a clearer understanding of potential consequences.

The Next Action Step: Gain insight and guidance through a complimentary and substantive consultation. We invite you to access our chat module, Schedule Your Complimentary Assessment, or call (866) 631-3470 to begin the process of evaluating your options, understanding potential tax consequences, and protecting your long-term financial interests.

Learn More About Expatriation, Exit Planning, and International Residency Changes

→ Expatriation and Exit Tax Planning

→ International Tax Planning

→ U.S. Expatriate Information Hub

→ Cross-Border Business Planning

Why Experience Matters in Tax Services

Tax matters often become more difficult when early decisions are made without understanding the full legal, financial, accounting, and regulatory consequences. A notice may appear routine. A reporting issue may seem minor. A business transaction may appear straightforward. An international investment may appear properly documented in another country. However, each of these situations can create exposure if the wrong information is provided, the wrong position is taken, or the broader implications are not evaluated before action is taken.

Tax matters often become more difficult when early decisions are made without understanding the full legal, financial, accounting, and regulatory consequences. A notice may appear routine. A reporting issue may seem minor. A business transaction may appear straightforward. An international investment may appear properly documented in another country. However, each of these situations can create exposure if the wrong information is provided, the wrong position is taken, or the broader implications are not evaluated before action is taken.

Experience matters because significant tax issues require more than technical knowledge. They require judgment, pattern recognition, familiarity with tax agency procedures, and an understanding of how tax, legal, accounting, estate planning, and business considerations affect one another. Allen Barron, Inc. and Janathan L. Allen, APC provide integrated guidance designed to help clients understand the issue, evaluate available options, and make informed decisions before avoidable consequences become more difficult to manage.

Attorney-Client Privilege and Confidential Guidance

Question: What Is the Attorney-Client Privilege?

Answer:

The attorney-client privilege is a legal protection that generally shields confidential communications between a client and their attorney when those communications are made for the purpose of seeking or providing legal advice.

This protection can become critically important in tax matters involving audits, reporting issues, financial exposure, investigations, disputes, or government inquiries.

This protection can become critically important in tax matters involving audits, reporting issues, financial exposure, investigations, disputes, or government inquiries.

The flat fact is this:

The IRS and other tax authorities can subpoena records, notes, emails, text messages, correspondence, working papers, and communications from your CPA, tax preparer, bookkeeper, financial advisor, or other third party.

Anything shared with them may potentially become evidence, and used against your interests.

That is one of the central protections provided by the attorney-client privilege. The modern day version of a strong castle surrounded by a moat.

When meaningful financial exposure, reporting issues, audits, investigations, or potential disputes exist, the distinction between legal counsel and non-privileged advisors can become extremely important.

Why Integrated Law, Tax, and Accounting Matters

Many business, financial, and tax issues are not isolated problems. They often involve overlapping legal, tax, accounting, reporting, operational, and strategic considerations that affect one another in important ways.

Many business, financial, and tax issues are not isolated problems. They often involve overlapping legal, tax, accounting, reporting, operational, and strategic considerations that affect one another in important ways.

A business transaction may create tax consequences.

A tax issue may affect accounting treatment.

An accounting structure may affect reporting obligations.

A legal decision may materially impact taxation, asset protection, ownership structure, or long-term business objectives.

The challenge is that many professionals evaluate these issues from only one perspective.

An integrated approach helps identify not only the immediate issue, but the underlying financial, legal, tax, accounting, and business considerations that may ultimately shape the outcome moving forward.

That integration has long been one of the defining advantages of Allen Barron’s approach to complex business, financial, legal, tax, and accounting matters.

Many business, financial, and tax problems initially appear to be isolated issues. In reality, they are often symptoms of a larger underlying challenge.

The old expression, “where there’s smoke, there’s fire,” frequently applies.

A business owner may believe they simply need a new entity structure, assistance responding to a tax notice, guidance regarding an international investment, or help evaluating a financial transaction. As the situation is examined more closely, other causational legal, tax, accounting, operational, reporting, or strategic issues often emerge beneath the surface.

An integrated approach helps identify not only the visible issue, but the underlying factors that may ultimately determine risk, opportunity, and long-term outcomes moving forward.

![]()

You Need Experienced Tax Counsel When the Stakes Are Significant

Janathan L. Allen has decades of experience representing businesses, business owners, investors, and individuals in IRS and California tax audits, payroll tax matters, worker misclassification inquiries, reporting issues, collection matters, and complex California tax controversies.

Her experience spans both proactive planning opportunities and high-consequence disputes involving the Internal Revenue Service, the California Franchise Tax Board, the California Department of Tax and Fee Administration, and the Employment Development Department.

Allen Barron also assists clients who are planning ahead, seeking to come into compliance, or addressing international tax concerns before they become larger disputes. Tax planning, voluntary compliance, offshore reporting, expatriate tax issues, international investments, and cross-border business activities often benefit from early, coordinated guidance. Taking the right steps now may help reduce exposure, preserve options, and prevent avoidable tax, legal, accounting, and financial consequences.

The initial consultation is a complimentary, substantive, confidential discussion designed to help you better understand your current position, the issues that may require immediate attention, and the strategies that may help protect your financial and business interests moving forward.

You are invited to engage the chat module on this page, contact Allen Barron, or call (866) 631-3470 to schedule a free, substantive consultation.

Learn more about Janathan L. Allen, APC and Allen Barron’s integrated tax, legal, accounting and business consulting services and how an integrated approach may help identify risk, protect assets, reduce unnecessary exposure, and support your long-term business and financial objectives.